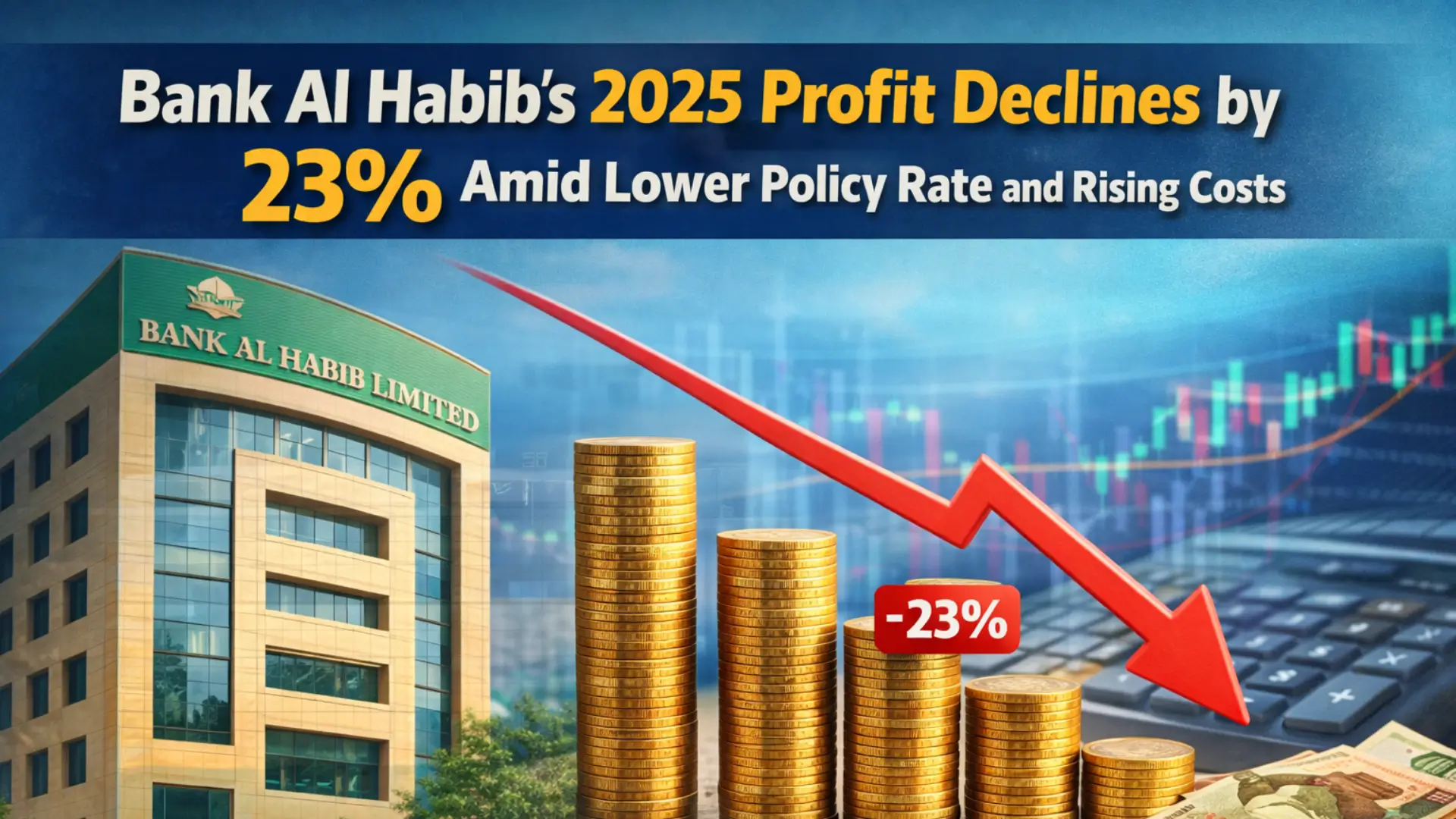

Bank Al Habib 2025 Profit Declines. Bank Al Habib Limited (PSX: BAHL) has announced its financial results for the year ended 2025, reporting a significant decline in profitability. The bank posted a consolidated profit-after-tax (PAT) of Rs. 32.46 billion, reflecting a 23 percent year-on-year (YoY) decrease compared to the previous year.

The decline in earnings has been attributed primarily to a reduction in the policy rate and a noticeable increase in operating expenses during the year. Despite the drop in profits, the bank announced a final cash dividend, offering some relief to shareholders.

Annual Financial Performance for 2025

For the full year 2025, Bank Al Habib recorded consolidated earnings of Rs. 32.46 billion, down from the previous year’s performance. The decline highlights the impact of changing macroeconomic conditions, particularly the easing monetary policy that affected asset yields and overall banking spreads.

The bank declared a final cash dividend of Rs. 4.5 per share for the fourth quarter of 2025 (4Q2025). This takes the total dividend per share (DPS) for 2025 to Rs. 15.0, compared to Rs. 17.0 paid in 2024. While lower than last year, the dividend payout indicates the bank’s continued commitment to rewarding its shareholders.

Fourth Quarter 2025 Performance Overview

In the final quarter of 2025, Bank Al Habib reported consolidated earnings of Rs. 5.8 billion, translating into an earnings per share (EPS) of Rs. 5.20. This figure represents a 23 percent decline on a year-on-year basis and a 16 percent decrease quarter-on-quarter (QoQ).

According to market analysts, including Topline Securities, the fourth-quarter results came in below industry expectations, mainly due to higher-than-anticipated operating expenses. The rising costs put additional pressure on profitability during the quarter.

Surge in Operating and Non-Interest Expenses

One of the key reasons behind the decline in profitability was the sharp increase in expenses. The bank’s non-interest expenses surged by 22 percent YoY and 4 percent QoQ in 4Q2025.

The increase was largely driven by higher marketing expenditures related to remittance services, as the bank aimed to strengthen its presence in the competitive remittance market. As a result, Bank Al Habib’s cost-to-income ratio rose to 67 percent in 4Q2025, reflecting the impact of higher operating costs on overall efficiency.

A rising cost-to-income ratio indicates that a larger portion of the bank’s income is being consumed by operating expenses, which can negatively affect profitability if not managed effectively.

Net Interest Income Declines Amid Lower Asset Yields

The decline in policy rates significantly impacted Bank Al Habib’s core income streams. The bank’s Net Interest Income (NII) for 4Q2025 stood at Rs. 31.4 billion, marking a 21 percent YoY decrease and a 5 percent QoQ decline.

The reduction in NII was primarily due to a fall in asset yields as interest rates softened. During 4Q2025:

- Interest earned dropped by 32 percent YoY and 7 percent QoQ to Rs. 77 billion.

- Interest expense declined by 38 percent YoY and 8 percent QoQ to Rs. 45 billion.

Although interest expenses also decreased, the sharper fall in interest income weighed heavily on the bank’s overall profitability.

Non-Interest Income Shows Mixed Trends

On a positive note, Bank Al Habib’s non-interest income increased by 3 percent YoY to Rs. 7.4 billion in 4Q2025, mainly driven by higher foreign exchange income.

However, on a quarter-on-quarter basis, non-interest income declined by 8 percent due to losses on securities during the fourth quarter. This mixed performance indicates volatility in non-core income streams, which can fluctuate depending on market conditions.

Effective Tax Rate and Profit Impact

The bank’s effective tax rate stood at 55 percent in 4Q2025, compared to 63 percent in 4Q2024 and 55 percent in 3Q2025. Although the tax rate improved compared to the same quarter last year, it remained relatively high, further limiting net profitability.

High taxation continues to be a challenge for the banking sector, as it reduces bottom-line earnings despite operational performance.

Stock Valuation and Market Position

From a valuation perspective, Bank Al Habib is currently trading at:

- A 2026 estimated Price-to-Earnings (PE) ratio of 7.2x

- A Price-to-Book Value (PBV) ratio of 1.2x

- A dividend yield of approximately 9.0 percent

These indicators suggest that while profitability has declined, the stock still offers an attractive dividend yield and reasonable valuation multiples compared to industry averages.

Conclusion

Bank Al Habib’s financial results for 2025 reflect the broader challenges faced by Pakistan’s banking sector amid declining policy rates and rising operational costs. The 23 percent drop in annual profit underscores the pressure on margins caused by lower asset yields and increased expenses.